Can a 'reserve currency' lose 80% value within a year?

Can a 'reserve currency' lose 80% value within a year?

The fall of Olympus DAO and its 'decentralised reserve currency'

Unless you’ve been living under a rock for the past 2 years, you would be aware of the ‘crypto moment’ we’ve landed into. ETH is up from $150 in Jan 2020 to $3,100 as of writing this piece (>2,000% return!), NFTs have become commonplace and everyone from Ranveer Singh to Ayushman Khurana is endorsing crypto projects. In fact, there are now over 20 million Indians holding crypto in < last 2 years, as compared to 50 million stock market investors till date.

Amidst all this craziness, this is my attempt to ‘Breakdown Protocols’. Coming from a traditional finance background (private equity), I believe there is a need to understand the fundamentals of a crypto protocol. Moreover, most protocols are likely to fail given the sheer abundance of new protocols launching and the industry being in a nascent stage. In this post, I will cover Olympus, a DAO working to build a ‘decentralized reserve currency’. At the time of writing, Olympus’ native token, OHM, is under pressure, and has lost over 80% of its market value. So if Olympus fails to bounce back, its journey could serve as an important learning for other DeFi projects out there.

We’ll cover the following aspects in this piece:

What is Olympus DAO building and what problem is it solving

Olympus inventions - Protocol owned liquidity and bonding

The DAO has fallen - What went wrong and led to over 80% decline in OHM’s market value

What could help OHM bounce back/ what are the learnings for other similar DeFi projects

So, let’s jump in!

What is Olympus DAO building and what problem is it solving

Over $150 billion of DeFi dollars are locked in stablecoins supply, an irony given that stablecoins reintroduce the dependencies and risks of the fiat system we are trying to leave, such as inflation, and centralized, unaccountable monetary policy. Stablecoins are pegged to the dollar, and the dollar is controlled by the US government and the Federal Reserve.

The core thesis of OHM relies on solving for the ‘Decentralization’ in Decentralized Finance (DeFi).

Olympus is a protocol that is building a community-owned decentralized financial infrastructure. Its native token, OHM, is a free-floating reserve currency, fully-backed by a basket of assets.

Now let’s break down this jargon.

Community-owned: Olympus works as a ‘Decentralized Autonomous Organisation (DAO)’, with ‘Ohmies’ using their OHMs to vote.

Free-floating: Similar to the idea of the gold standard, OHM provides free-floating value determined by market sentiment

Fully-backed: Unlike DAI or USDC which are pegged to the value of the U.S. dollar, OHM’s reserves are crypto assets held by the Olympus Treasury. Each OHM token is backed by 1 DAI in the treasury.

In summary, the protocol is aiming to create a currency to compete with the dollar - a "non USD pegged stable asset" that is backed by crypto instead of fiat currencies.

Initially, the treasury consisted of just DAI, with every OHM issued having 1 DAI in the treasury as its backing. However, the protocol has since expanded the treasury to include other assets, such as FRAX, another algorithmic stablecoin, as well as OHM-DAI LP tokens from SushiSwap, and OHM-FRAX LP tokens from Uniswap.

Olympus inventions - Protocol owned liquidity and bonding

What is unique about this protocol? What led to OHM’s market map growing to $4 billion within six months of launch?

Currently, the biggest challenge for DeFi protocols is liquidity, often described as “toxic liquidity”. Initial high rewards lure the liquidity providers (LPs), but as the protocol matures and rewards normalize, the LPs remove their liquidity, causing token price fluctuations. The protocol gets stuck having to pay out rewards in its own token. Paying out liquidity rewards can cause inflation as additional tokens are minted to boost liquidity, thus decreasing the value of the tokens in the market.

Olympus sought to solve this challenge and introduced ‘Protocol Owned Liquidity’. This is a new paradigm, as previously protocols rarely owned their liquidity as explained above.

Olympus achieves this through a process called ‘Bonding’.

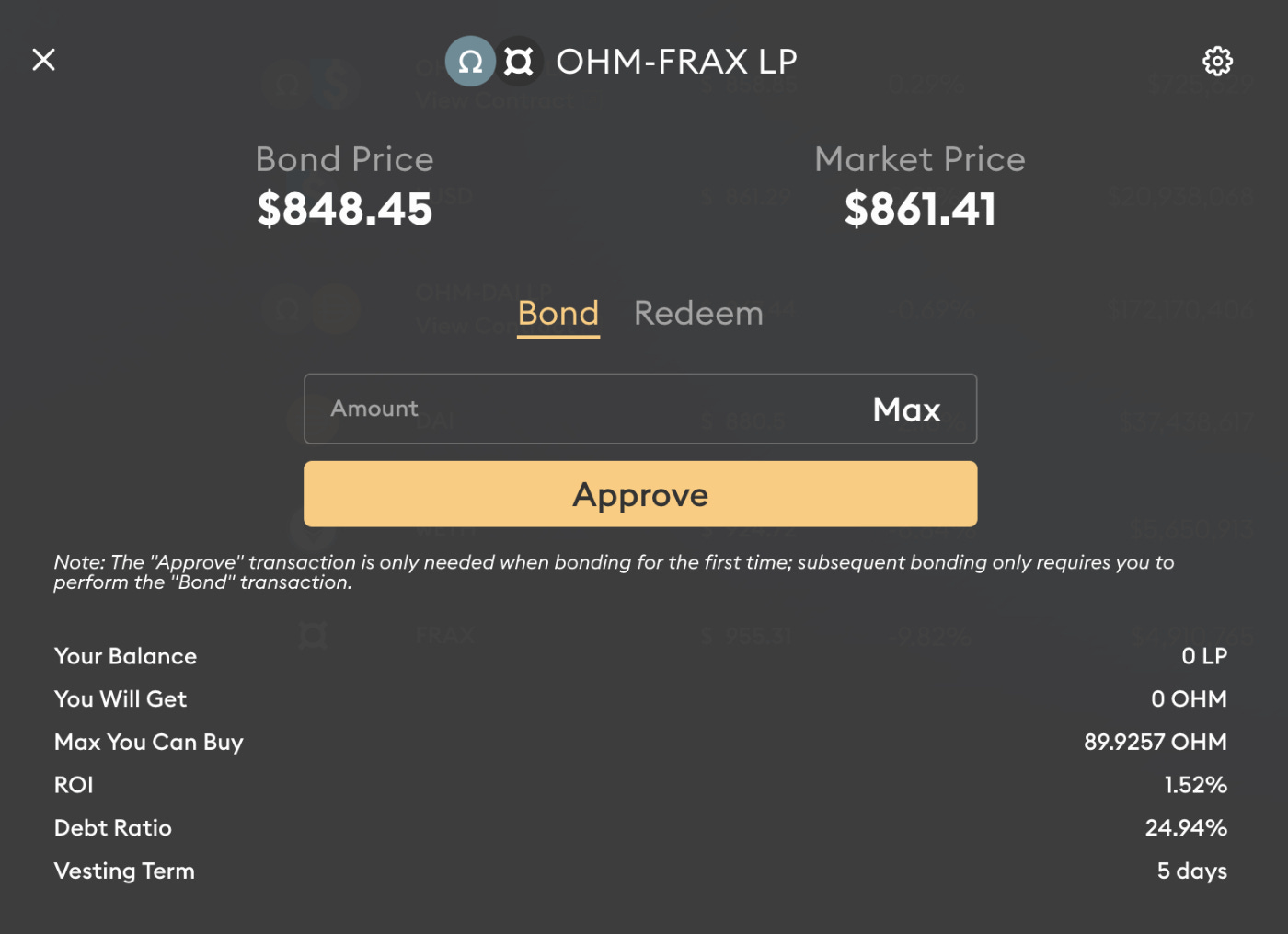

The Olympus bonds program buys Olympus LP (liquidity pool tokens) and other assets from investors in return for discounted OHM tokens. Here’s how it works.

Let’s say you wanted to invest $5,000 into OHM. For most tokens, you would just go to SushiSwap and buy $5,000 worth and that would be the end of it.

But for OHM, you have another option. Instead of buying $5,000 of OHM, you can buy $2,500 of OHM and $2,500 of FRAX, fund the OHM-FRAX liquidity pool, and then sell that liquidity position to Olympus for a bond.

At any time, Olympus is willing to pay you OHM tokens in return for selling them liquidity. In this case, you get a 1.52% return over 5 days for selling them your OHM-FRAX LP. So instead of getting $5,000 of OHM if you had bought it directly, you’ll now get $5,076 worth of OHM! Sure you’d earn some fees holding the LP tokens, but you won’t make 1.52% in 5 days.

This is one of the main ways new Olympus tokens are issued, and it ensures that every Olympus token is backed by tokens and liquidity stored in the treasury. And it’s how Olympus owns almost all of its liquidity.

Protocol-owned liquidity through bonding is the monetary policy lever that led to the protocol becoming a top-5 DeFi protocol by market cap within months of launch.

To learn more about Olympus fundamentals, check out Olympus FAQ section and this Bankless article. For a detailed understanding of bond prices, check out this primer on Bonding.

If you haven’t already, do subscribe to our newsletter 👇

So what went wrong?

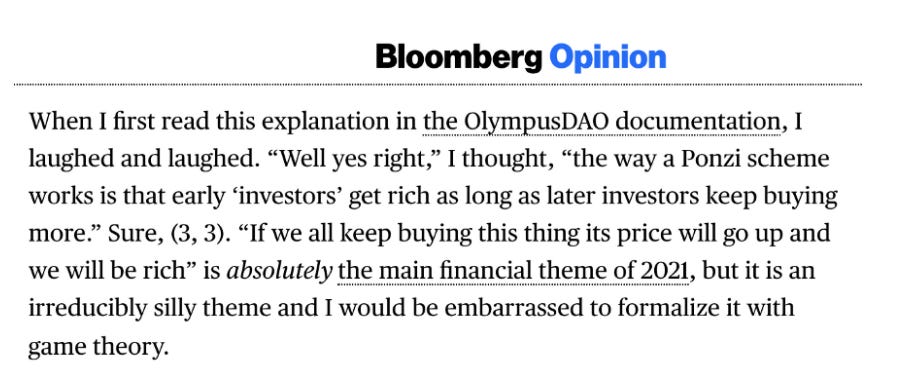

Critics have been divided in their opinion about Olympus since its inception. Some call it a ‘Ponzi’, since the core functionality of 3000% APR via new OHM token mints is unsustainable to the point of being fraudulent. Treasury uses the profits from subsequent investors (through bonding) to payout high APY staking rewards to earlier investors, making it sort of a pyramid scheme.

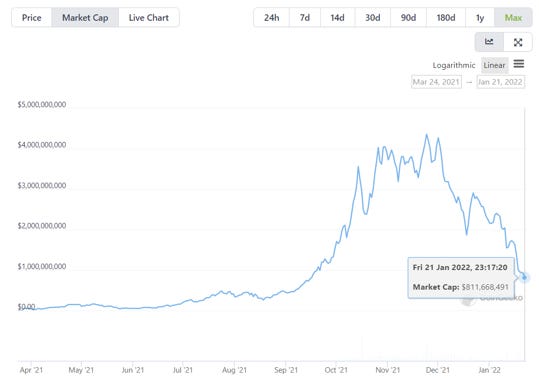

While few on the other hand opined Olympus to be one of the most important protocols in Defi, such that it could even replace Bitcoin or become the reserve currency of the internet. At its peak, Olympus was a top-5 DeFi protocol by market cap, and grew to $4 billion market cap within six months of launch.

As we noted above, the market cap of Olympus is down to less than a billion, or more than 80% from its peak of $4 billion.

Key to the project’s success was staking and allowing the protocol to own its liquidity. Staking led to locking up more of the supply, theoretically reducing selling pressure. As of 15th Dec 2021, 97% of the supply was being staked. It's currently around 85%. But clearly, this was not enough to prevent holders from selling eventually.

While the broader crypto market has remained volatile in 2022, the OHM slump can be attributed to 5 major reasons:

Massive profit-taking from major OHM holders: While no official statement is issued by Olympus, according to data from Etherscan, one OHM holder swapped over 82,500 OHM tokens worth more than $11 million on 17th Jan’22, causing the market cap to drop 30% in a day. The trade happened on SushiSwap with the OHM tokens traded for the stablecoin DAI.

Unsustainable growth in market cap: Olympus' market capitalization grew 15x in 2 months (from $260M to $4B). People don’t necessarily need to be project supporters to make money. After this big runup, those who were all about making quick money dumped the token.

The Ponzi narrative becoming stronger…

The epic trilogy "Of Smoke and Mirrors" proceeds with the rare sequel that is even better than the original- 𝗣𝗮𝗿𝘁 𝟮: 𝗧𝗵𝗲 𝗚𝗼𝗱𝘀'𝗙𝗮𝘁𝗵𝗲𝗿 A Masterclass on building your own Ponzi empire; The Caveman Classic; Learning the 10 cOhmandments; medium.com/@game_theorizi…

The epic trilogy "Of Smoke and Mirrors" proceeds with the rare sequel that is even better than the original- 𝗣𝗮𝗿𝘁 𝟮: 𝗧𝗵𝗲 𝗚𝗼𝗱𝘀'𝗙𝗮𝘁𝗵𝗲𝗿 A Masterclass on building your own Ponzi empire; The Caveman Classic; Learning the 10 cOhmandments; medium.com/@game_theorizi…

…..even in mainstream media:

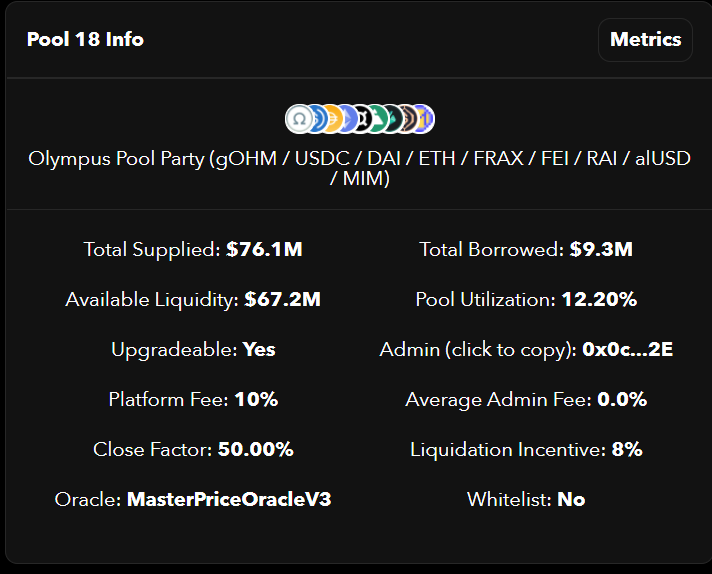

Leverage trading on OHM tokens: In particular, users were using Fuse, an interest rate product by Rari Capital, to borrow cryptocurrencies against their OHM holdings. Pool #18 on Fuse is focused on Olympus, locking up over $76 million across OHM and nine other cryptocurrencies. The pool takes OHM staking a step ahead for users: unlike staking OHM on Olympus, staking OHM on Fuse allows users to borrow cryptocurrencies against their OHM holdings while continuing to earn interest on the staked OHM. This allows users to access liquidity without having to sell their OHM rewards and missing out on potential gains.

Huge price drops are catastrophic for leverage trades. Users liquidated their overleveraged OHM long positions to cut losses, further causing the price to decline and leading to a cascade of liquidations that ultimately led to further downward pressure on the token price.

Proliferation of forks: Numerous Olympus forks have emerged with specific themes incorporating climate goals (Klima), Metaverse (Hunny, Rome), NFTs (OpenDao), Ecosystem (Wonderland Frognation) etc. The quick cash-grabs narrative of these forks slowly started to sink in people's minds as if that was what Olympus was trying to achieve.

I joined the Olympus DAO few days back to understand how the community was reacting to the fall. The community remains strong, in execution phase with multiple initiatives planned, such as Olympus Pro, Olympus Grants, V2 Bonds. They have now more than 40 partnerships in their ecosystem, including their recent migration of liquidity to Balancer and to Copper Launch. The DAO also holds regular AMAs, which are also streamed on Twitch. With a strong community, active contributors and sound governance practices, Olympus can bounce back, but the chances are slim in my opinion.

What could help OHM bounce back/ Learnings for other projects

The flywheel (or pyramid scheme) created by OHM tokenomics seemed to have turned in the wrong direction. If you observe the flywheel highlighted by Ryan Watkins in his tweet below, if the market turns bearish or one of the flywheel components goes sideways, the whole *wheel* can start to cycle backward. And that is what seems to have happened recently.

Few thoughts on what could help OHM emerge stronger/ learnings for other similar DeFi projects:

Revisit the ‘decentralized reserve currency’ narrative: Olympus argues that bitcoin and eth are too volatile and USDT is susceptible to the whims of U.S. monetary policy, so therefore will depreciate over time. So Olympus created a reserve currency (like Dai), backed by assets (like Dai), but not pegged (except for the floor price). So basically this currency free floats to the upside, and is backed by the treasury. But how would that help in making it a decentralized reserve currency? Until now, nothing is priced in OHM. No markets or DEXes have real OHM adoption. And none of the initiatives seem to be geared towards this narrative - the existing initiatives are focused on staking/ earning rewards through rebasing. Moreover, a reserve currency should not be so volatile from a utility perspective.

Strengthen the treasury to prevent future liquidations, while minimizing risky exposures of high leverage trades

Implement a mechanism to disincentivize people who stake and dump. It could be done by either rewarding long-term stakers or implementing time locking systems similar to veCRV.

For those looking to understand the technicals behind this conundrum, check out the thread below:

What do you think about OHM - wagmi or ngmi? (Sorry folks, I am also new to crypto :P)

If you are a Web3 noob (like me) and would like to learn together, do hit me up on Twitter/ LinkedIn.

To get more such pieces delivered straight to your inbox, subscribe to our newsletter and give us a shoutout! 👇